5 Actions to take for a successful do-it-yourself credit fix

If you don’t know where to start your credit fix, here are 5 simple actions that will give you some direction.

1. Check your credit reports

To get a better understanding of your credit picture you must review your credit reports from Experian, Transunion and Equifax. Annualcreditreport.com offers free credit reports once a week. But they don’t offer credit scores. myFICO offers credit reports and FICO scores for a fee you can get anytime.

Once you have your credit reports do the following:

- Review the credit reports for errors and inaccurate information. Here are several tips on how to dispute negative credit.

- If you find information that is incorrect, send a credit dispute letter.

- Make sure you don’t have outdated information reporting. Outdated information can easily be disputed and removed.

2. Clear up charge-offs

One charge-off can take up to 150 points off your credit score. It can be detrimental to your credit scores compounded by the fact that months before your account was officially charged off, a number of late or missed payments occurred. Missed payments alone can significantly damage your credit.

Ways to remove a charge-off from reports:

- If the account has been sold to a debt collector, the original creditor must report a zero balance. If this is not the case, dispute the original creditor and request a deletion from your credit reports.

- Review the outstanding balance. If it’s more than you think it should be, dispute it and request a deletion. The creditor may simply correct the balance but it doesn’t hurt to request a deletion.

- Verify the charge-off date on the original account. The charge-off date should be the date of your first delinquent payment on the original account. Dispute the charge-off and request a deletion for any incorrect dates surrounding the account.

- Convince the creditor to remove the charge-off from your credit report in exchange for payment. There is no law that mandates creditors report your account information at all. The laws state that if information is reported to the credit bureaus, that information must be accurate.

3. Clear up debt collection accounts

Debt collection accounts have a big impact on your credit scores too. It makes it even worse when you have the original creditor reporting late payments and a charge-off. Your scores are doubly impacted. The best action for collection accounts is to get them removed from credit reports. Paying a collection account will not help your scores.

Ways to remove debt collection from reports:

- Ask a collection agency to remove the collection account from their credit reports in exchange for payment.

- If paying is not an option request debt validation. Ask the debt collector to prove you owe the debt.

- Dispute any inaccurate information surrounding the collection listed on your reports.

4. Improve your payment history

Payment history is one of the major components of your FICO scores. Late and missed payments will reduce your scores, and bankruptcies, public records and collections can cause significant damage. Negative information will remain on your credit report and impact your credit scores for 7-10 years. On time payments will have a positive impact on your credit scores.

Steps to take to improve your payment history:

- Bring accounts current

- Continue to pay on time

- Once you’ve caught up on payments and demonstrated a continued ability to pay on time, request your creditor remove the late payments as a goodwill gesture.

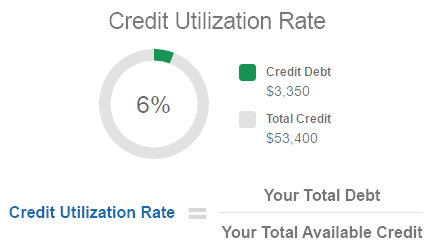

5. Pay down credit card balances

The next major component of your credit score is credit utilization rate. FICO scoring models take into account how much you owe compared to how much credit you have available. This is called credit utilization rate or balance-to-limit ratio.

Basically it’s the sum of all of your revolving debt (such as your credit card balances) divided by the total credit that is available to you (or the total of all your credit limits).

When you use a lot of your available credit your credit scores take a huge hit. The typical school of thought on how much of your available credit to use is around 30 percent. However, FICO has said in the past that people with the highest credit scores typically use no more than 7 percent of their available credit.

For example, if you have a $10,000 credit limit across all of your credit cards, you should try to keep your total credit card balances below $700 to keep your credit utilization rate low.

Here are ways to reduce credit utilization:

- Reduce your debt by paying off your account balances.

- Request a credit limit increase on an existing account or open a new account. But you must not use the additional available credit – that will defeat the purpose.

Once you reduce or pay off debt remember to keep the account open. The FICO scoring model factors in the age of your oldest account and the average age of all of your accounts. Consumers with longer credit histories are rewarded.

Stay up-to-date with your latest credit score information and learn what lenders know about your scores.