Credit repair is tedious and time-consuming. How long it takes to improve credit scores or reach credit goals varies from person to person. Becoming a member of the excellent credit club can be a long process.

But whether it’s 6 to 12 months, or 2 years, the time it takes to improve credit scores is worth every letter, phone call, frustrating, gut wrenching, victorious moment.

The good news is once you take the time to improve credit scores, you’ll reap the benefits in ways never imagined.

Just think about it – you apply for a mortgage, car, student or business loan, apartment or something as simple as a cell phone contract – no more crossing your fingers hoping to be approved. You have the assurance that your credit files are clean and your scores are poppin’…no matter what the decision.

That’s a great feeling, knowing you have blemish-free credit and whether you are approved or denied, bad credit played no part in the decision. You can’t beat that type of stability and peace of mind. You may not be able to control credit approvals but you can for sure control your credit scores.

A reader once asked what they could do to improve credit scores because their daughter had to drop out of college due to lack of money. The daughter’s scholarship funds were not renewed and the financial aid office suggested student loans.

The student had a limited credit history and a co-signer was needed. Unfortunately, not one person in the family; grandparents, aunts, uncles, or close family friends was able to co-sign due to poor credit.

Excellent credit is invaluable. While I don’t advocate loading up on student loan debt, it’s heartbreaking when a student is forced to drop out as a result of poor credit.

It’s in your power to have excellent credit and here are the steps:

A healthy Savings Account is tantamount to excellent credit

1. Build up your savings account. If your goal is to improve credit scores, remember that having a healthy savings account is as important as having excellent credit. Money in the bank is tantamount to excellent credit and here is why.

Credit issues arise from people unable to pay their credit obligations. Whether it’s job loss, medical emergency, long-term illness, major home or car repairs – life events happen.

It may take 6 to 12 months or longer to recover from a loss of income. In the meantime, your credit obligations continue. Start building emergency savings. This should be separate from your college, retirement or investment savings.

If you think you don’t have extra money to contribute to an emergency savings account, think again. Consider reviewing your monthly obligations to eliminate unnecessary expenditures. There are things you can live without like monthly subscriptions: cable, Sirius, Netflix, Hulu, Pandora, Birchbox, wine club…you get the picture.

Perhaps less dining out, specialty coffees, beer or liquor. Cutting back is not for a lifetime. It could simply be for 12 months or until you build an emergency savings. Since the national savings account interest rate is 0.17 percent, it’s worth considering a high-interest savings account to make the most of your money.

The journey to excellent credit requires living on a budget

2. Live on a Budget. To improve credit scores you must live on a budget. Only when your credit goals are reached, consider adjusting your budget, but until then, adhere to a fairly rigid budget during the journey to excellent credit scores; or, if you don’t like budgeting consider a side gig to earn extra money.

Hloom, a professional services site, surveyed 2,000 Americans to compile a report on the United States of Financial Waste, which looked at how people in the U.S. waste their hard-earned dollars. The findings analyzed wasteful spending habits of Millennials, Generation X(ers) to Baby Boomers. It was interesting to see that all 3 generations put the most wasteful spending on dining out. But as you can see below the 3 generations differed on other wasteful expenditures.

Rebuilding credit involves using credit, not building debt

3. Build credit, not debt. You don’t need to carry debt to improve credit scores. Unfortunately, not everyone rebuilding credit understands this concept. Part of rebuilding credit means using credit. Credit cards are certainly not the only tools to accomplish this but they are the most expedient tools. Consistently charging small amounts to a credit card and paying off the balance on-time and in-full each month is what helps build excellent credit over time. Not only do you show how well you can manage a line of credit, you also create a positive payment history.

Be vigilant in not building debt. That means you use credit cards for small purchases that can be repaid in full every month. Be mindful that credit cards will help you develop an excellent credit history but it’s all too easy to charge more than you can afford and end up with a balance that can be a struggle to repay.

At least 3 credit cards should be reporting to credit bureaus monthly

4. Open 3 credit cards. If you have only negative credit reporting to the credit bureaus, open 3 credit cards to start building excellent credit. For people who currently have positive credit cards reporting, skip to No. 5 below.

Keep in mind your scores may see a slight drop due to hard inquiries but it won’t impact scores for long. Even though credit inquiries remain on your credit report for 2 years, FICO Scores only consider inquiries from the last 12 months in calculating scores.

Plus, the benefits your credit history receives from having positive accounts reporting far outweigh any temporary score deduction due to hard inquiries. In fact, many people experience a score boost just by having positive tradelines reported; especially if no other credit card accounts report positively.

If you’re wondering what creditors offer easy to qualify for accounts, consider the following credit cards that report to the 3 major credit reporting agencies:

opensky® Secured Visa® Credit Card. Boost your credit score fast—2 out of 3 opensky® cardholders see an average increase of 47 points after 6 months. They have an 89% approval rate with zero credit risk to apply! Simply deposit as little as $200 to establish your credit limit. The only drawback is your deposit doesn’t earn interest. Plus, earn up to 10% cash back on everyday purchases. The interest rate is currently 24.39% (variable). Deposits are fully refundable.

First Digital Mastercard®. This is an unsecured card that has no minimum credit score requirements. While it’s an easy card to qualify for, it comes with fees. You may find better options at your bank or credit union. But if you’re still interested the First Digital Mastercard® is available to people with fair, poor, or limited credit. The online application process takes a few minutes and you’ll get a response in seconds. Unsecured credit cards for bad credit typically come with program and annual fees already attached to the card, not to mention higher interest rates.

Upgrade Visa. See if you quality in minutes for the Upgrade Select Visa that acts as a line of credit. There are no fees with credit lines ranging from $500 to $20,000. You can use wherever Visa® is accepted. See if you qualify in minutes without hurting your credit score, plus, get access to a virtual card while you wait for your card to arrive in the mail.

All of these credit accounts should be considered starter cards for rebuilding credit only. After 6 to 12 months you will be able to qualify for unsecured credit cards with rewards and higher credit limits. It’s never a good practice to load up your credit file with these type of starter cards with low limits. Credit card issuers tend to mirror the credit limits you currently have when approving accounts. Lots of small limit accounts may hinder the possibility of larger credit limits.

Practice the credit habits of people with excellent credit

5. Zero balance on all cards except one. When FICO published a report on the habits of people with excellent credit, they found that consumers with 7% or less utilization of available credit had the highest credit scores. To improve your credit scores during the rebuilding process, keep a zero balance on all cards except one. The one credit card that reports a balance should have a 7% or less balance but more than $2.

For example, if you have a $200 credit limit card it should report somewhere between $2 and $14. The other cards must report $0. That means you will need to pay them in full before your balance is reported to the credit bureaus.

The strategy is rigid but if you want the best possible scores during the rebuilding process, this is the way to go. Once you reach credit goals and improve credit scores, you will have much higher limit cards to choose from which means you can spend more even while practicing this strategy.

Keep in mind, the FICO scoring system rewards people that keep as much space as possible between account balances and credit limits. But, when you have a credit file reporting a $0 balance on all credit accounts, it indicates that you’re not using your credit. Not using credit may cause a big dip in scores.

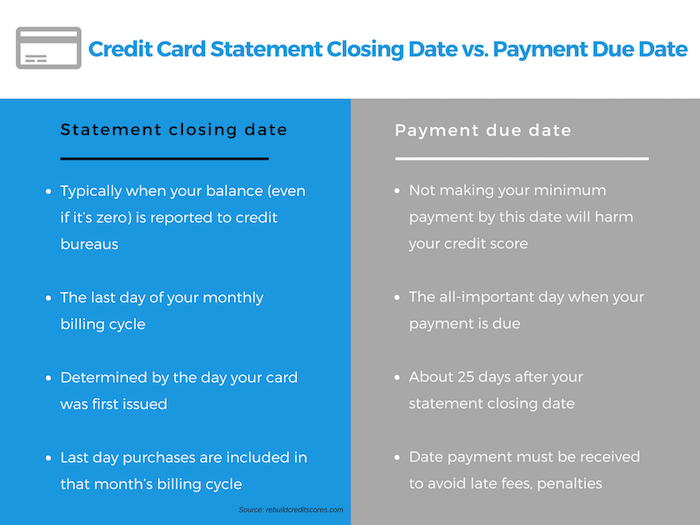

Timing is everything – Keep track of credit reporting dates

6. Keep track of credit reporting dates. In order to maintain a zero balance on all cards except one you must know when your credit cards report balance information to the credit bureaus. This is simple to do because most credit cards report to the credit bureaus on the statement closing date. The statement closing date is separate from your payment due date.

For example, if you have a payment due date of January 15th then typically the statement closing date will be approximately 3 days after the payment due date. The balance on the statement closing date will report to the credit bureaus.

In other words, if you have a payment due on the 15th with a $60 balance, you should pay the balance down to approximately $2 to $14, assuming your credit limit is $200. Remember the other 2 credit card accounts should be paid in full by the statement closing date as well because you want a zero balance on all cards except one.

The statement closing date is the date your utilization should be at 7% or less. If a credit card company allows you to choose payment due dates, consider aligning credit card due dates with your pay dates that way you can ensure your account balances will be paid in full or at 7% when on your statement closing date which reports to the credit bureaus.

Keeping track of your statement closing date and payment due date puts you in control of your credit scores. For instance, make larger purchases the day after your credit card statement closing date to get the entire next billing cycle before a payment is due. That’s approximately 25 days without interest being assessed to your account.

Maxing out credit cards is a credit score killer

7. Never max out credit cards. Using credit cards wisely is beneficial to improve credit scores plus excellent credit can make many of life’s financial situations easier and less costly. Maxing out just one credit card will kill a credit score immediately after the maxed out balance is reported to the credit bureaus. The second largest part of your credit scores (30%) is amount owed. This category is basically the credit utilization ratio. Credit utilization ratio is how much total debt you have versus how much credit is available.

Using 100% of your available credit means you’ve maxed out. But it’s worth noting FICO scoring models take into account both your overall utilization (across all of your cards) and the individual utilization on each card.

Although it may differ for some credit profiles, it seems as though 88.9% utilization is the threshold when FICO dings your score. That means if you allow any one card to report more than 88.9% utilization one month, your score will take a huge dive even if the other cards are not maxed out.

If you have no choice and must carry a balance, spread the balance over 2 or 3 credit cards. You want any one credit card to report less than 30% otherwise FICO will ding you for that cycle until it’s paid down.

Credit utilization only includes your revolving credit accounts, such as credit cards. It doesn’t consider other types of credit like auto, personal or mortgage loans. The good news is damage to your score is temporary if you bring the balance down and never pay late.

Credit experts have long suggested avoiding a credit utilization rate of above 30% but while you are pursuing credit goals to improve credit scores, you want to follow No. 5 above – Zero balance on all cards except one.

Set-up minimum payment with Autopay

8. Never miss a payment with autopay. Setting an automatic payment of at least the minimum amount due is a good safety measure. Payment due dates could easily slip your mind. You may be traveling or just really busy and forget a payment. Autopay is a lifesaver.

Of course to improve credit scores you’re going to pay more than the minimum to keep your credit utilization low. But there’s no excuse to ever miss a payment with autopay.

If you setup autopay make sure your bank account has enough funds. The last thing you want is an automatic payment causing an overdraft fee. Consider opening an online free checking account just for paying bills.

As a rule, it’s good to bank at more than one financial institution; so why not utilize a separate free checking account for pay bill payment only. Once you have the separate account open it’s easy to setup a small direct deposit to that account to ensure funds are available for autopay. Setting an automatic payment of at least the minimum amount due is not only a good safety measure to avoid late fees, but more importantly, to avoid damage to your credit scores.

Establish a banking relationship with a real bank or credit union

9. Benefits of knowing your banker. This is for people that don’t have a traditional checking or savings account. If you’re currently using a prepaid debit card to conduct financial transactions, open a real bank account. Even if you have a negative ChexSystems or Early Warning Services Report, or bad credit, get back into banking.

The benefits of having a bank account will complement your excellent credit goals:

- Banks typically offer an array of financial products that at some point in time you may need. For instance, mortgage, car or personal loan. Small business financing, credit cards, higher interest CDs.

- Bank customers that have established a good banking relationship can often gain access to better interest rates than what is advertised to the general public. It’s called “relationship pricing” on loans and savings products.

- Depending on the size of your overall relationship, you may be able to get higher rates on your CD deposits and lower rates on loan products.

- Banking with a financial institution that is familiar with your finances can be extremely helpful when it comes to planning for the future. Your banker can identify opportunities to enhance your financial position with savings, retirement and investment products.

- If you’re planning to purchase a home by financing, most mortgage brokers will want to see bank statements. Prepaid debit card statements may not be sufficient.

Get back into traditional banking if you’ve been shut out. Find banks that don’t use ChexSystems or banks that offer second chance checking accounts. It’s typically pretty easy to get an online checking account with banking tools to help you budget, free bill payment, mobile deposits, free ATMs nationwide, along with a dedicated team of bankers for online customers.

Pursue strategies to get rid of negative credit items

10. Recent negative credit items should be disputed first. Negative items on credit reports typically remain from 7 to 10 years. The most recent 2-year negatives are impacting your credit scores more than older negative items. Tackle the most recent negatives before disputing older negative credit items. In fact, older negative items matter much less than recent negative items.

Consider the following strategies for negative credit:

- How to dispute charge-offs

- Pay for delete collection accounts

- Dispute collection accounts

- Dispute late payments

- Remove tax liens and judgments

- Request goodwill adjustments for late payments

- Request goodwill adjustments for paid charge-offs

Although people have experienced success with online disputes, old-fashioned US Mail is still the best dispute method. Credit dispute letters and goodwill letters in writing increase the chance a human person will actually read the credit dispute. Plus, you want to avoid any type of negotiation of a pay for delete or goodwill adjustment over the phone. Your request in writing is proof along with a response from the credit bureaus, a creditor or debt collector.

Be patient, there is no quick fix to improve credit scores if you have multiple negative items. It took time to get into trouble, it’s gonna take time to get back on track.

Installment loans vs. Revolving credit cards

11. Create a good mix of credit. FICO looks at your mix of credit cards, retail accounts, installment loans, finance company accounts and mortgage loans. Having credit cards and installment loans with a good credit history will improve your credit scores. Credit mix is one of 5 categories when calculating a credit score. It accounts for 10% of your score.

Installment loans are personal, auto, mortgage or student loans that are repaid over time with a set number of scheduled payments. Revolving credit is credit cards, retail credit accounts, lines of credit, such as a home equity line of credit (HELOC). With revolving credit, you have the option to either pay the balance off in full at the end of each billing cycle or to carry a balance over from month to month.

Having just one type of account (all credit cards) in your credit profile may limit how much you’ll be able improve credit scores. If you want to gain points in this category showing that you can manage a mix of credit types is beneficial.

An installment loan added to credit profiles will only help if you don’t currently have an installment loan reporting (mortgage, personal, auto or student). Adding an installment loan can be done with a secured loan.

Secured Credit Builder Loans. Credit unions are the best choice for secured loans because many offer “credit builder” loans where your deposit qualifies you, not your credit scores. Typically, you can open a credit builder secured loan with as little as $500. The strategy would be to get the secured loan, then pay it down. For example:

(1) Deposit $500 as collateral to secure the loan;

(2) Credit union gives you $500 in loan proceeds;

(3) Make a $460 payment on the loan;

(4) Pay the remaining $40 over the next 6 months or so; and

(5) Once the loan in paid in full, the credit union releases your deposit.

What you accomplish by this strategy is to reduce your overall installment amount owed in comparison to the original installment loan borrowed. This can give your credit scores a boost.

Adding an active installment loan and immediately paying it off to less than 9% remaining balance can give a FICO 08 scoring model an increase. Most lenders use FICO 8 scoring models even though FICO 9 scoring models have been available since 2016. If you already have active installment loan this will not have the same impact.

Credit builder loans are a great choice to improve credit scores because these loans are small and manageable. Plus, you build credit relationships with a credit union or bank that goes a long way in future lending needs. You build a solid foundation for mortgage, personal, auto, student and even business loans.

Self Lender Credit-Builder Loans. You don’t always need upfront money for a credit builder loan. Self Lender Credit- Builder loans allow borrowers to make monthly payments for 12-months. The monthly payments are deposited into a FDIC-Insured Certificate of Deposit Account. Payments are reported to the major credit bureaus Experian, Transunion and Equifax.

At the end of 12-months your money is returned to you, plus you have 12-months of on-time payment history. It takes about 5 minutes to open a Self Lender account. Even though a credit report is not pulled, ChexSystems is used to determine approval. You can’t have had a negative ChexSystems report, such as bounced checks or unpaid fees, in the previous 180 days. Check out Self Lender if you lack the up-front collateral for a credit builder loan.

Unsecured personal loan. If you need the proceeds of a loan immediately, you’ll need to take an unsecured personal loan at a higher interest rate. Don’t take out an unsecured loan if you cannot afford to make on-time monthly payments. Rebuilding credit history to improve credit scores does not include making late payments or worse, defaulting on credit obligations. Read the fine print on bad credit loan offers and make sure you can pay a bad credit loan off early, without penalty, to avoid the high interest.

Conclusion

Excellent credit makes the difference in access to financial products necessary to finance a car, purchase a home, attend college or grow a small business. There are very few basic aspects of life that wouldn’t benefit from having excellent credit scores, including renting an apartment, paying for car insurance, signing up for utilities and even landing a job.

It all starts with building a savings account before or during the process of rebuilding credit. An emergency fund will go a long way in preventing late payments if job loss or illness occurs. Remember to have a budget, no matter your income, to keep track of unnecessary spending and contribute to your savings, investment and retirement.

Secured credit cards for rebuilding will be the easiest to qualify for because your deposit ensures approval. Using secured cards for 6 to 12 months will qualify you for better, higher limit, rewards credit cards.

Pay credit cards before the statement closing date to ensure a low or zero balance reports to the credit bureaus. In simple terms, don’t pay your credit card by the due date just to turn around and charge items right away. Those new charges will show up on the credit bureaus plus cause your credit score to drop for high utilization.

Work on ridding your credit report of negative credit items. Be patient, it takes time, but it’s time well spent and worth the credit journey.

Get started on reaching credit goals today.