Dealing with bankruptcy on credit reports is complex. There are several strategies that will give you an idea of how to remove a bankruptcy from your credit reports, get professional removal help and rebuild a better credit scores.

Removing a bankruptcy from your credit reports is somewhat complicated because bankruptcy is a legal action which dismisses you in part or in whole from your debts.

A Chapter 7 bankruptcy proceeding is deleted from your credit reports 10 years from the filing date. A Chapter 13 is deleted from your credit reports 7 years from the filing date.

After you file bankruptcy make sure all of your creditors and accounts which were included in the filing are listed on your credit reports as “included in bankruptcy.” If not, the creditors, late accounts, collection accounts and charge-off accounts will continue to be listed as due and owing which will severely lower your credit scores.

Disputing a bankruptcy and getting it removed is difficult. It may be a waste of time disputing a bankruptcy as “not mine”, especially when it really is yours and can be easily verified.

But verifying disputes based upon facts is not as easy.

Disputing facts such as filing date, balance of liabilities, type of bankruptcy, social security number, discharge dates on debts, type of accounts and even docket dates are a lot harder to investigate.

There are a few ways to dispute bankruptcy listings that may work. First, remember that credit reporting agencies verify records through a third party database such as PACER, LEXIS NEXIS, INNOVIS, SAGESTREAM or ARS.

Even though credit reporting agencies will list the bankruptcy court as the “furnisher” of information, no one at the credit reporting agency actually contacts the bankruptcy courthouse where the proceeding was filed. This fact is what you can use to attempt to remove bankruptcy from your credit reports.

Several strategies to remove a bankruptcy from credit reports

1. Inaccurate Reporting. Look for incorrect reporting of facts and dispute the listing. It may get deleted and no further work is necessary. A bankruptcy must be listed accurately in your credit reports.

2. Method of Verification. If the listing gets verified and remains you have the right to request the credit reporting agencies’ method of verification. Request the credit reporting agencies send you the following:

- Name of the courthouse;

- Person’s name they verified the dispute with;

- Address;

- Telephone number; and

- Documentation used to verify the dispute.

The CRA’s must respond to your request within 15 days and provide the information. Undoubtedly they will only respond with the name and address of the courthouse. But this is good.

3. Follow-up Letter to Credit Reporting Agency. Now you can mail another letter to the credit reporting agency and let them know you contacted the court and were informed they do not furnish records and information to the credit reporting agencies, which they do not.

Can you imagine the time and legal ramifications if court clerks spent the time to personally verify and follow procedures of the Fair Credit Reporting Act. The courts rarely, if ever, verify public records with credit reporting agencies according to the FCRA. The only time when bankruptcies are verified at the court level is when a person or service is sent directly to the courthouse to review public court records.

4. Get your Proof in Writing. In order to create your paper trail you may wish to send a letter to the court administrator of the courthouse where the bankruptcy was filed. In your letter request what their procedure is for verifying records with the credit reporting agencies. When sending court clerks any letters ALWAYS INCLUDE A SELF-ADDRESSED STAMPED ENVELOPE if you want a response.

Depending on their response, you will have proof on paper that the actual courts do not verify information directly with the credit reporting agencies. Now take that letter from the court and follow-up with another letter to the credit reporting agency with your proof the courts do not verify bankruptcy filings.

5. Request a Deletion. Should the credit reporting agency respond by telling you they are not required to give you that information, they have violated the FCRA. If the credit reporting agency does not respond within 15 days they have violated the FCRA and the entry must be deleted.

The FCRA, Section 609 a (2) regarding disclosures provides leverage to get the item deleted. You can request to see what they used as proof to verify the bankruptcy and if they are unable to provide it, the bankruptcy must be deleted. The credit reporting agency must disclose the source of the information.

Also, FCRA, Section 611, paragraph (6)(B)(iii) regarding procedures and results of reinvestigation states “…if requested by the consumer, a description of the procedure used to determine the accuracy and completeness of the information shall be provided to the consumer by the agency, including the business name and address of any furnisher of information contacted in connection with such information and the telephone number of such furnisher, if reasonably available…”

Credit reporting agencies are required to conduct investigations of disputed items with the “furnisher” of information. The Bankruptcy Court should be the furnisher of information, not a third party source such as PACER or LEXIS NEXIS.

Vigilant nagging and challenging the credit bureaus on the method of verification process may be the best way to get a bankruptcy removed, but there are no guarantees.

If the credit bureaus continue to verify the bankruptcy and refuse to provide you with the method of verification other strategies are:

- File a small claims lawsuit for violations of the FCRA

- Submit a Complaint with the Consumer Financial Protection Bureau

- File a complaint with your State’s Attorney General (find your state’s attorney general)

Let the professionals handle bankruptcy removal

As you have read removing a bankruptcy from your credit report is possible; however it’s time consuming and complicated. Consider enlisting the help of a credit repair company to navigate the process for you. Credit repair companies are highly experienced at disputing negative items on your credit reports.

Getting bankruptcies removed is one of their specialities along with the accounts “included in bankruptcy” like charge offs and collections.

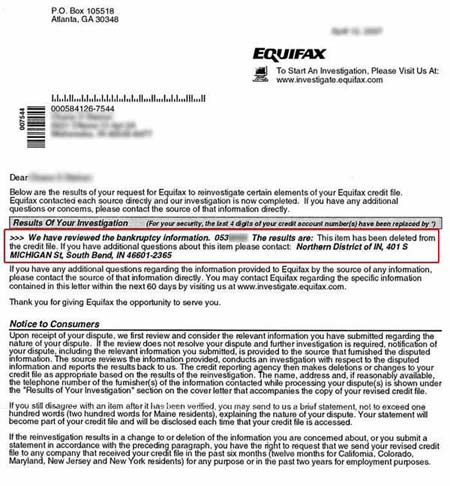

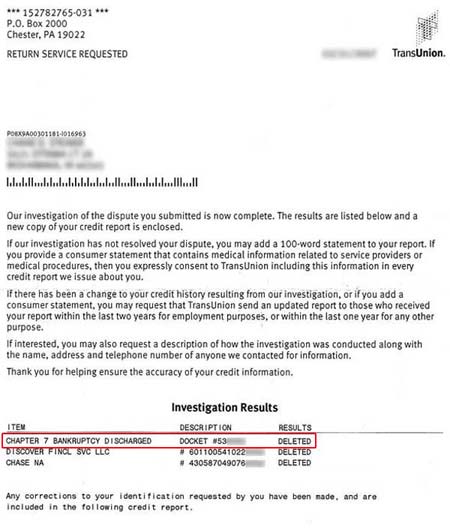

Lexington Law has over 25 years of removing negative credit from consumer credit reports. In fact, in 2017 Lexington Law boasts over 10 million REMOVALS in 2017. That number includes bankruptcies. Look at the example below.

Call Lexington Law at (877) 587-4574 for a free consultation on bankruptcy removal, a free credit report and score. If you’re tired of getting turned down for credit, let the professionals at Lexington Law Firm handle it for you. All types of negative items can be removed from credit reports, including including bankruptcies, foreclosures, repossessions, charge offs, late payments, judgments, tax liens and more.

Concentrate on Steps to Rebuild Credit After Bankruptcy

Begin re-establishing your credit as soon as possible after a bankruptcy. There will be fewer options and some credit card companies and banks will deny an application when a bankruptcy is listed on your credit report. But start with secured credit cards where you deposit a specific amount in an FDIC-insured account and your credit limit is equal to what you’ve deposited with the card issuer.

If you belong to a credit union ask about a credit builder loan or use a service like Self Lender where you can build credit through a secured loan without having the money upfront. A personal loan is an installment loan and this can really boost credit scores.

Make sure the card reports your payment history to all three major credit bureaus. As you begin to repay on time, your good payment history will be factored into your credit score and the sting of bankruptcy will matter less.

As more time passes the negative effect of bankruptcy will diminish as long as you continually pay all of your bills on time. Bankruptcies on credit reports take on less significance as the filing becomes older. In fact most banks, lender, mortgage companies and auto dealers know consumers with a bankruptcy can some times be a better credit risk because they have less debt and a clean slate.

But to enjoy new credit you’ve got to immediately take steps to rebuild credit after bankruptcy.