One of the major reasons to consider alternatives to Chime is the enormous amount of complaints when compared to licensed banks that have way more customers like Chase, Bank of America and Wells Fargo.

Don’t get me wrong, these large banks have their share of complaints but when compared to Chime, it’s a little off-putting.

Numerous Better Business Bureau Complaints

Considering Chime has over 22 million customers, in the last 3 years they’ve amassed over 8,076 complaints with the Better Business Bureau (BBB).

When compared with Wells Fargo, a bank with 68 million customers and a well-documented record of unethical practices, Chime has managed to garner more BBB Complaints in the last 3 years.

- Wells Fargo customers have filed 6,389 total BBB complaints in the last 3 years.

- Bank of America has over 69 million customers and their BBB complaints total 7,721 in the last 3 years.

- Chase, America’s largest bank, has over 80 million customers with a total of 4,818, BBB complaints in the last 3 years.

Chime may indefinitely hold customer deposits

May 7, 2024, the Consumer Financial Protection Bureau (CFPB) issued the penalty after finding that Chime delayed thousands of customer refunds for weeks and sometimes up to 90 days, inflicting significant financial harm on individuals who simply wished to close their Chime accounts.

The Bureau found that Chime’s conduct was unfair in violation of the Consumer Financial Protection Act of 2010. The order requires Chime to come into compliance, pay a $3.25 million civil money penalty, and pay at least $1.3 million in redress to consumers.

Here is one such complaint to Chime on Facebook where they refuse to refund a customer’s $14,000 balance after 4 months of funds being held:

Chime does not handle customer complaints fairly

Feb. 27, 2024, the California Department of Financial Protection and Innovation (DFPI) entered into a consent order with Chime regarding the accuracy and responsiveness of Chime’s handling of customer service transactions. Chime was ordered to pay $2.5M in penalties and improve customer service standards due to unfair complaint handling.

Here is a 2023 Twitter post regarding Chime’s handling of a customer complaints:

Chime customers have reported being denied a refund after the investigation and if they were granted a provisional credit, that amount is later debited from their accounts.

Hi Well, I had unauthorized transactions on my account on my Chime account and I tried to get them disputed and y’all team won’t give me my money back. Yeah I cancelled my cards and got sent send new cards and all my transactions are being denied so I talked to a lawyer.

— Yah’Lay (@yahlaymusic) July 20, 2023

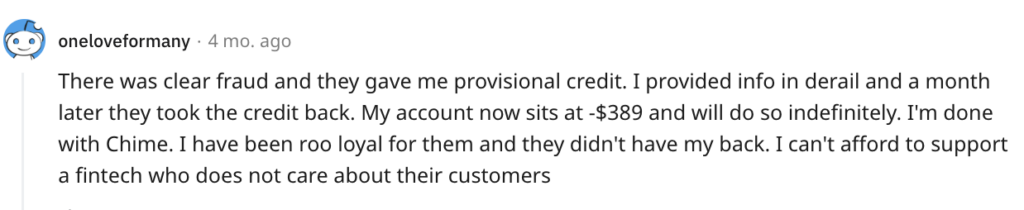

Here is a Reddit post regarding the reversal of provisional credit.

Chime’s History of Closing Accounts Without Warning

A 2021 Propublica study found that Chime closed or froze customer accounts when potential fraudulent activity was thought to have occurred. These actions were carried out without any prior warning, leaving customers in the dark and without access to funds.

It was found that a significant number of account closures were triggered by the company’s suspicion of fraudulent federal stimulus checks and unemployment insurance deposits. What’s worse is Chime had actively promoted opening accounts with these specific types of funds through an extensive marketing campaign.

Confused customers made complaints and sought answers as to why their accounts were abruptly shut down but Chime failed to offer satisfactory explanations. Only after facing significant backlash, Chime admitted to making “mistakes” in handling the situation and acknowledged the mishandling of customer accounts.

![]()